ARGENTINA – Update on Curupi Pora farm activities (June 2023)

Situation/weather: We have now entered in winter season but with unusually mild temperatures for the period. It’s very strange or unusual to see the farm so “green” during this time of the year. We could register some good rains in May which help the recovery of pastures after the drought period faced earlier this year again. The farm is currently in good shape and we are entering winter in very good conditions.

Cattle operation: We have currently above 6,300 heads at the farm. We are in the peak season for cattle sales. This year, we have planned to sale over 1,600 animals.

Below, you can see some pregnant cows (spring service of 2022).

Here, some heifers 2 years old which will enter into spring service in October 2023.

Below, you have some cows with their baby calves which are going to be weaned in July. You will also see some cows that have just finished fall service (April/May 2023).

ARGENTINA – Update on Curupi Pora farm activities (March 2023)

Situation/weather: We are still suffering from heat waves and lack of rains (light rainfall evaporates immediately due to the heat). This is the 3rd consecutive year that Uruguay, south of Brazil, Paraguay and Argentina are experiencing La Niña weather phenomenon. Please see the Article from La Nacion dated 13/03/23 which addresses the impact and consequences of this situation. We were not affected by fire as it is the case in several farms in the region, and overall the farm has decent pasture in comparison with other neighbouring farms.

Cattle operation: We have currently above 6,800 heads at the farm, of which 2,060 spring calves. Around 50% of them are males which are going to be sold. 900 female are going to be kept for internal reposition and the other will be available for sale. By end of March, we will perform pregnancy test of spring service.

Here you can see some cows and baby calves almost 6 months old (around 180 kg/head). We are preparing 1st sales of this cycle with 240 male calves.

Here you some heifers of 18 months which will enter in service by end of this year. You can see that they are in very good condition.

To assure optimal water distribution and availability for the cattle, we are currently building a new water tank. You can see here the basement of the construction.

Paraguay – Rice harvest at Salitre Cue farm (March 2023).

Rice harvest has restarted at the farm. We are expecting a good harvest in terms of yield (> 7 t/ha) and quality as we didn’t faced any water shortage during the irrigation period considering our seeding strategy.

Given the hydrological forecasts for the season and boom in input prices, we have decided with our partner GPSA only to sow 390 ha of rice for this cycle. Indeed, we were right given the drought faced in the region. We could fully mitigate our risk by using the water of our artificial lake of 480 ha to fully irrigate for the entire period our rice fields. Paraguay, South of Brazil, Uruguay and Argentina faced one of the worst droughts in recent memory which will deeply impacts farm exports. For example, the Buenos Aires Grain Exchange forecasts a further 20% drop in soybean and corn production for the season.

As a result of the drought, paddy prices should be at a high level for this season.

ARGENTINA – Update on Curupi Pora farm activities (January 2023)

Situation/weather: Heat waves are back! Temperatures reached stifling highs, exceeding 40°c in many provinces.

Hot, dry weather and low humidity levels are also creating dangerous fire conditions. Fire-fighters are already mobilized to fight against fires as you can see.

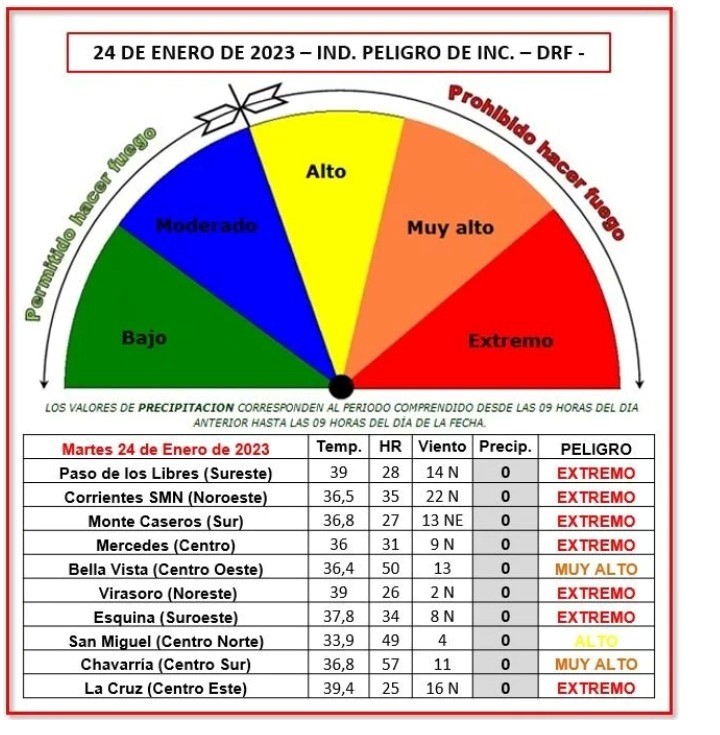

We are not exempted in Corrientes region as the situation has been classified under extreme vigilance by the authorities for forest or brush fires. Our staff is under permanent alert to control small events. For bigger, we need the support of the fire fighters with their equipments.

Cattle operation: We have currently above 6,800 heads at the farm, of which 2,000 are calves. Heat stress can strongly impact the animals at various levels (well-being, production, diet, fertility, etc.). To management this stress, we are adjusting food supply (silage, completed with corn and pellets).

Meat prices have recently increased by 30% (ie supermarket prices) to adjust to inflation as they were so far below the inflation level on the local market (see article from LaNacion dated 24/01/23). So, producers are expecting further increase of meat prices they get in the coming months (up to 20%).

Grassing area has reducing given the lack of water. You can see the very low level of the river Santa Lucia which is bordering our farm.

This year, we have subleased to a contractor 200 ha where corn has been sowed. We will be paid in kind as we need corn to feed our heard. As you can see, the contractor started his harvest.

PARAGUAY – Update on Salitre Cue farm activities (January 2023).

Situation/weather: We have recently registered some heavy rains so as in Argentine Mesopotamia (Misiones, Corrientes, and Entre Ríos) and also in southern Brazil which fit for once with our irrigation period of the rice. The region is again facing the consequence of La Niña weather pattern. Lot of concerns have already expressed after the downspout at the Paraguay River nears its third consecutive all-time low. The low water level has a direct impact on navigability, which, in turn, raises freight costs.

Rice: Given the hydrological forecasts for the season and boom in input prices, we have decided with our partner GPSA only to sow 390 ha of rice for this cycle. If for whatever reason we would face any shortage in rains or pumping restriction on the river, we could fully mitigate our risk by using the water of our artificial lake of 480 ha to fully irrigate for the entire period our rice fields. So far, the weather gave us reason.

All rice fields sowed are in very good conditions as you can see. We are in the pick of the irrigation period and have a very uniform crop.

Corn: In addition to rice, we have decided with our partner to sow 488 ha of corn this year as a rotation to soybean. We are in the process to finish with the sowing and the crop is emerging in the early field sowed as you can see.